Ten years after banking crisis, Americans still feel ripples

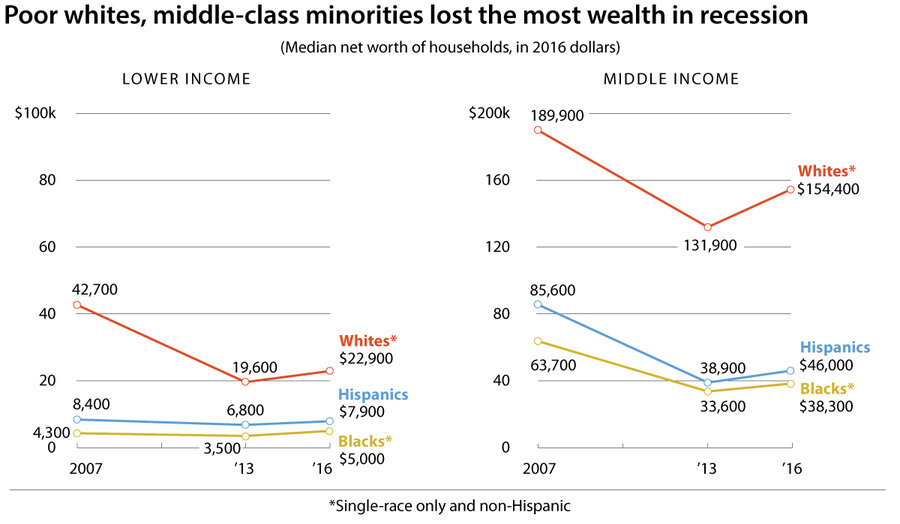

Ten years ago this week, the US investment bank Lehman Brothers collapsed under the weight of high-risk real estate investments gone bad. That signaled the most dire phase of a financial crisis that had already been simmering. And it spurred policymakers toward all-out fiscal and monetary support for the financial system, which staved off a potential chain reaction of bank failures. But if a second Great Depression was averted, the crisis took a lasting toll on American households. An investor-fueled housing bubble went bust. More than 5 million Americans lost homes, and many more saw their net worth plunge along with home prices. “I couldn’t keep up,” says Shirley Thomas, an African-American grandmother in Brockton, Mass. A foreclosure-prevention program helped keep her in her home. As of 2016, median net worth was still well below 2007 levels, with middle-income black and Hispanic-American households especially hard hit alongside lower income white households (see chart). Many families have made progress. But Anne Depew, of the Boston-area foreclosure prevention program, says that “so many Americans are just one hardship away from disaster.”

Why We Wrote This

The financial crisis that erupted 10 years ago is a reminder of linkages and interdependence. Global investors became the spark, yet lasting impacts still linger for many Americans.

After buying her Brockton, Mass., home in 2005, Shirley Thomas had to work three jobs to make the $3,000 monthly payment. When she was so overworked she had to give up one of the jobs – grocery shopping for the elderly – she began to fall behind on her mortgage payments.

That’s when the foreclosure walls began to close in.

“I couldn’t keep up,” says the African-American grandmother.

Why We Wrote This

The financial crisis that erupted 10 years ago is a reminder of linkages and interdependence. Global investors became the spark, yet lasting impacts still linger for many Americans.

Like Ms. Thomas, many Americans went through the wringer of the Great Recession and came out poorer on the other end. A decade later, many still have not made up the lost ground. It wasn’t just the loss of income or jobs – the stuff of every recession – that made the downturn so bad. It was the concurrent financial crisis and the resulting flood of foreclosures that caused many Americans to lose their homes and, as a result, their wealth.

Unlike income, wealth is harder and usually slower to amass, involving paying off a mortgage or building up a business. As of 2016, the latest figures available, the typical American household’s wealth had still not recovered. In 2007, it had $139,700 in inflation-adjusted dollars; by 2016, it was only $97,300.

And the recovery has been uneven. In general, black and Hispanic families were hit especially hard, and their recovery since the crash remains especially far from complete. Poor whites, too, saw severe losses – with median net worth in 2016 at half its 2007 level.

“It's really only upper income families that have recovered,” says Rakesh Kochhar, a senior researcher at Pew Research Center, a nonpartisan think tank based in Washington. At lower incomes, “whether you are white, Hispanic, or black, your wealth in 2016 was less than what you had before the recession.”

When financial services firm Lehman Brothers filed for bankruptcy on Sept. 15, 2008, it triggered the darkest phase of a financial crisis that ripped through the banking system. Investors worldwide had already shifted from bullish to panicked, as a boom in dodgy mortgages was seen to have tainted the prospects of US financial firms. When Lehman went bust, without a buyer or emergency government funding to support it, the entire financial system seemed at risk.

The stock market plunged, as did home prices. Borrowers who had recently bought homes, often with mortgages that required little or no down payment, found they owed more than their homes were worth. Banks increasingly foreclosed on delinquent borrowers.

The long tail of a banking panic

Between 2008 and 2014, the US experienced 5 million outright foreclosures, according to ATTOM Data Solutions, an Irvine, Calif., firm that tracks real estate. That total doesn’t include the forced sales of homes and “short sales” where lenders accepted a loss on mortgage debts. Whatever equity people had built up in their homes was often lost.

Lower-income African-Americans, though pummeled by the loss of income and jobs during the Great Recession, were spared somewhat from the loss of wealth – partly because so many were renters rather than owners, with little net worth to begin with. By 2016, they were one of the rare groups to be doing better than before. Lower-income Hispanics followed a similar path, though not yet a full recovery. (See chart.)

Pew Research Center, based on Federal Reserve survey data

Middle-class Hispanic households, by contrast, lost more than half their wealth, and in 2016 the median was 46 percent below the pre-recession level. Middle-class black households saw a slightly smaller decline and now are down 40 percent. While middle-income white households weren’t hit as hard, the typical lower-income white household saw a 44 percent dive in wealth. (One reason lower-income whites were more affected than lower-income minorities is that they are far more likely to own a home.)

Overall, the wealth gap between whites and minorities increased between 2007 and 2013, according to the Pew study. The white-to-black wealth ratio for middle-income households rose from 3-to-1 to 4-to-1 and the white-to-Hispanic ratio from 2-to-1 to 3-to-1. The gaps between upper-income families and all other income groups, minority and white, now stand at record highs.

Foreclosures and recovery on Main Street

Brockton, a poor and diverse city in Plymouth County south of Boston, followed the national trend. The rate of homes in the county receiving a foreclosure notice quintupled between 2006 and 2008. While the rate never got near some boom-and-bust areas like Las Vegas’s Clark County, Plymouth nevertheless led the state in the rate of foreclosure filings from 2009 through 2015.

“Brockton was the epicenter of the foreclosure crisis in Massachusetts,” recalls John Buckley, the county’s register of deeds. “Home prices rocketed downward. So a lot of people lost value in their assets,” even those who didn’t get foreclosed on.

By 2016, the city’s already high poverty rate had worsened for blacks and Hispanics. It stayed level for non-Hispanic whites.

Since then, real estate has boomed and the job market is so strong that companies are starting to raise pay. Nationally, income for the typical US household rose to a record $61,400 last year, after adjusting for inflation, although the figure is not statistically different from 2007, the Census Bureau reported Wednesday. But black household income fell slightly last year, after two years of solid growth.

The recovery of wealth could be slowest for many at the bottom rungs of the income ladder, although analysts are reluctant to speculate. “It takes wealth to gain more wealth,” says Valerie Wilson, an economist with the Economic Policy Institute, a liberal think tank in Washington. “It could take another several decades and maybe longer than that, depending on where we’re going in terms of policy.”

Thomas counts herself fortunate. Although her bank was preparing to foreclose, a foreclosure prevention program called the SUN Initiative, stepped in to buy the house. The home was valued close to $400,000 when Thomas bought it in 2005. The group convinced the bank to sell it for $120,000 and then resold it to Thomas. Now, Thomas’s mortgage payment is $1,500.

“It’s half of what I was paying before,” she says. Thomas figures her financial position has recovered from the Great Recession's impact. “I’m not worse off…. Now, I'm down to one [job].” Next year, she plans on retiring, “but I’m not going to fully retire,” she adds.

The SUN Initiative, one of the programs of impact-investing firm Boston Community Capital, has nearly 60 borrowers in Brockton who were saved from foreclosure.

“We don't think of them as high-risk,” says Anne Depew, general manager of the initiative, which operates in seven states. “We are talking about people who are school teachers, police, firefighters. It shows that so many Americans are just one hardship away from disaster.”